In January 2023, ViaBTC Capital and CoinEx jointly released the 2022 Crypto Annual Report to offer data analysis and insights into nine sectors, including Bitcoin, Ethereum, stablecoins, NFT, public chains, DeFi, SocialFi, GameFi and regulatory policies. This report also predicts the crypto trend in 2023.

According to the report, affected by factors such as the macro environment and bull-to-bear transition, the whole cryptocurrency industry became bearish in 2022. In particular, following the Terra meltdown in May, most cryptocurrency sectors were hit by the bearish impact. Below is the overview of each segment.

1. Bitcoin

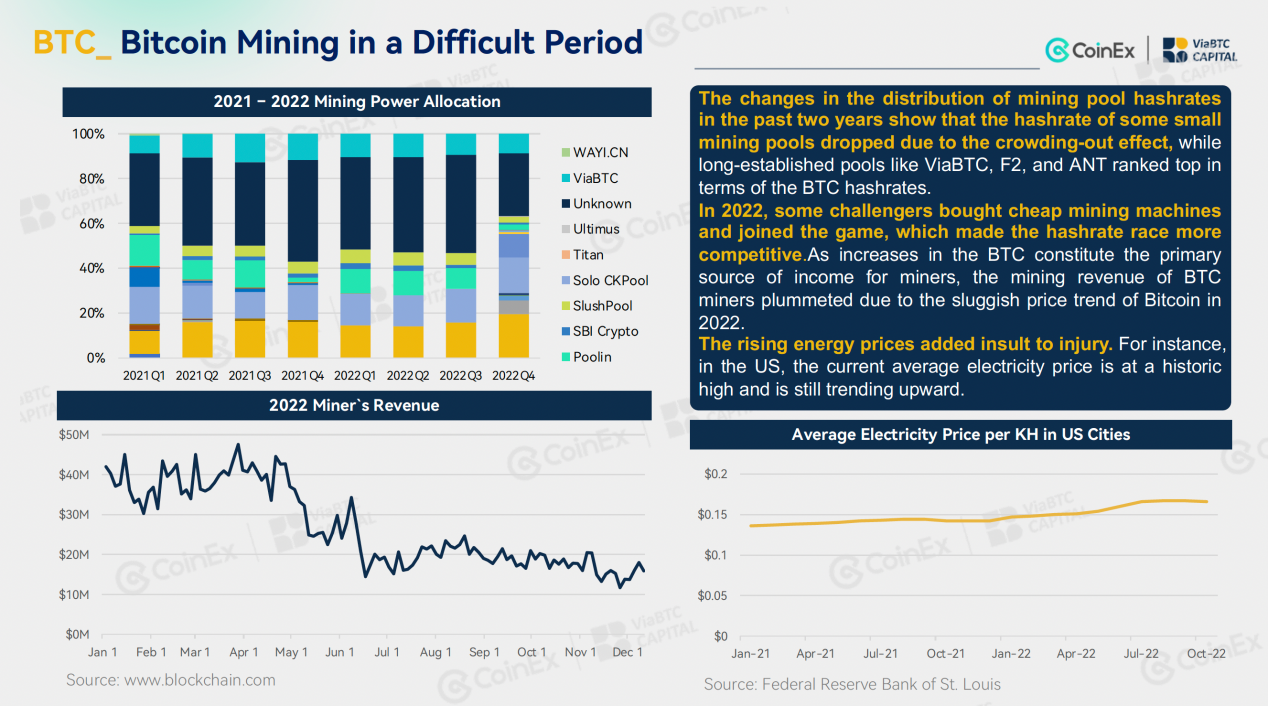

In 2022, the overall performance of Bitcoin remained sluggish, with significant declines in price and trading volume compared to 2021. The price at the end of 2022 even fell below the peak of the last bull market. The price trend of Bitcoin throughout the year is obviously influenced by the pace of US interest rate hikes, but as the US interest rate hike policy continues to advance, its impact on the price of bitcoin is gradually diminished. Regarding BTC mining, the network difficulty remained at a historic high. Meanwhile, the mining revenue plummeted, and miners have had to shut down their old models. Affected by multiple factors, the mining industry witnessed a strong crowding-out effect, which drove owners of small mining farms out of the market for various reasons. At the same time, long-established mining pools and mining farms managed to maintain a certain level of stability.

2. Ethereum

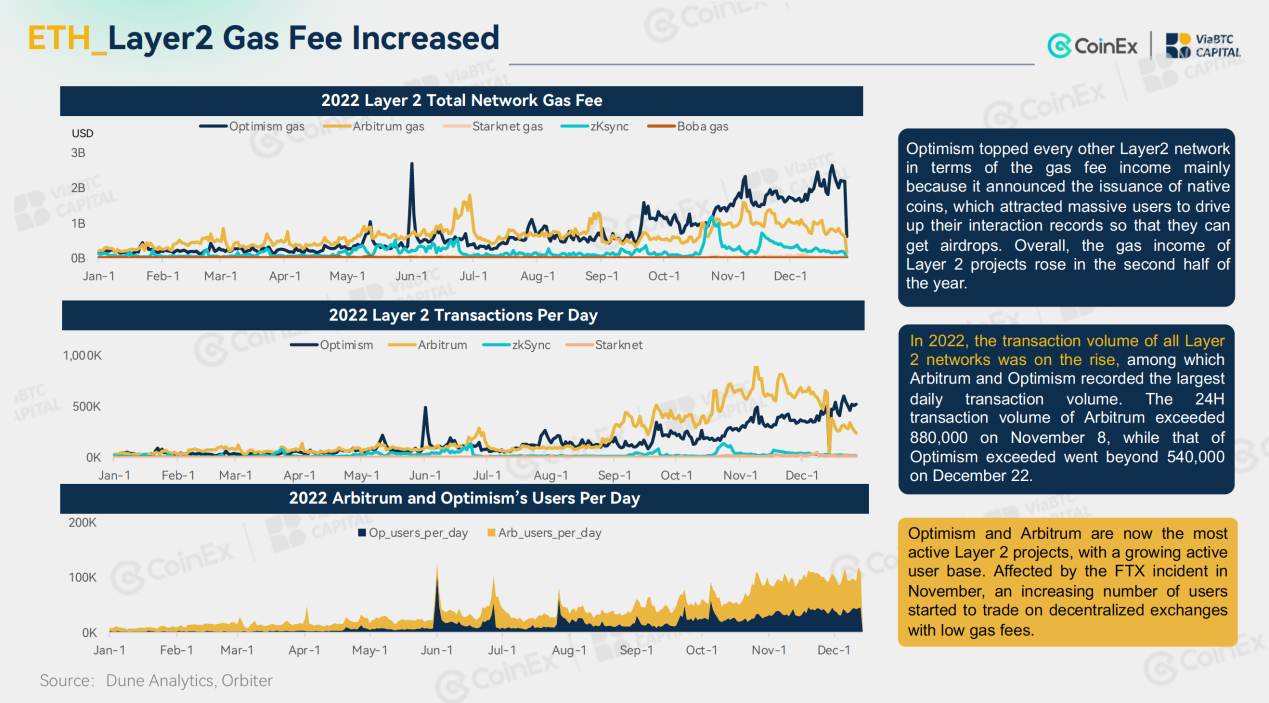

The primary statistics of Ethereum trended downward in 2022. In addition to the secondary market price and transaction volume, the on-chain data, including TVL, transaction cost, active address and burning volume also took a plunge. Despite that, the network did achieve a lot of progress in 2022. On September 15, Ethereum completed the historic transition from PoW to PoS. The Merge significantly cut the network’s energy consumption and daily output, thereby reducing the dumping pressure from secondary markets. Meanwhile, Layer 2 projects such as Arbitrum, Optimism, zkSync, and Starknet launched their mainnet either in whole or in part. Although their daily transaction volume was far less than Ethereum mainnet, the projects exceeded Ethereum in terms of the number of addresses. Moreover, their gas fee was generally 1/40 of that charged by Ethereum. At the same time, the network also saw an exponential increase in gas fees during 2022.

3. Stablecoins

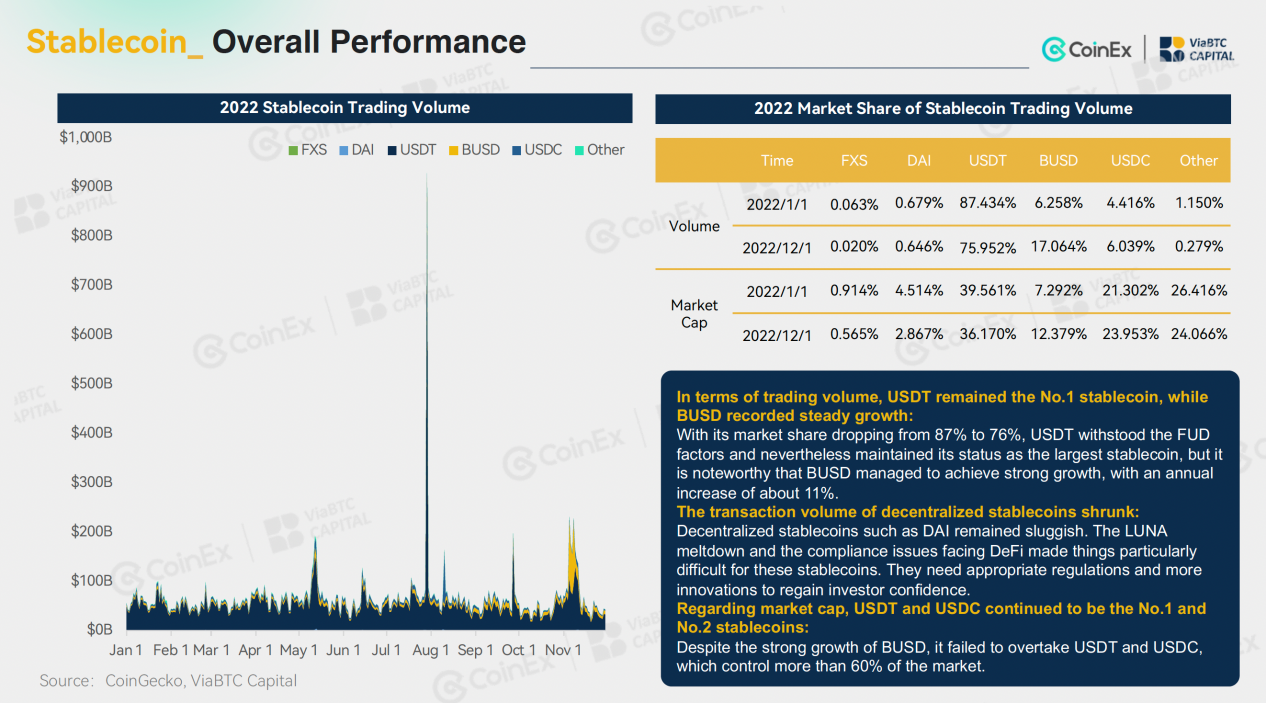

The stablecoin market as a whole was stable in 2022. Specifically, throughout the year, the supply of stablecoins fell from $157 billion to $148 billion, a 6% drop. In this regard, the fall was not substantial. With respect to centralized stablecoins, USDT maintained its dominance, while BUSD is growing rapidly on Binance’s back. By contrast, algorithmic stablecoins were hit hard by the fall of LUNA, which shattered the faith in decentralized stablecoins and reduced trading volumes. As a result, there was a clear drop in the number of new decentralized stablecoins.

4. Public chains

Despite the rough market conditions in 2022, public chains remained a competitive sector. Due to the overflow of demand caused by the congestion of the Ethereum network, the new public chain with low fees maintained a bright performance before May. However, as various bad news brewed and fermented, a series of bankrupt occurred one after another. Many public chains were greatly impacted, and the decline was even worse than that of Ethereum. In May, Terra collapsed in only a few days, making it the first well-known public chain to fall. Furthermore, the Terra meltdown was also a signal that the market turned fully bearish. In November, hit by the fall of FTX and Alameda Research, Solana’s token price and TVL took another plunge, and the projects within its ecosystem were also hurt. Other new chains such as Fantom and Avalanche were also struggling. At the same time, a number of new public chains, including Layer 2 projects like Arbitrum and Optimism and Meta-related chains such as Aptos and Sui, made their debut in 2022.

5. NFT

Last year, the NFT sector declined after its initial boom. In April, the market cap of the NFT reached $4.15 billion, a historic high; In May, driven by the boom of Otherside, a metaverse NFT collection developed by Yuga Labs, the trading volume of the sector hit a record high of $3.668 billion. But soon afterward, as the NFT market turned sluggish, the trading volume declined. Meanwhile, the price of blue-chip NFTs, as well as the ETH price, plummeted, which both negatively affected the market. On the other hand, the number of NFT holders kept growing and reached a historic high in December.

6. DeFi

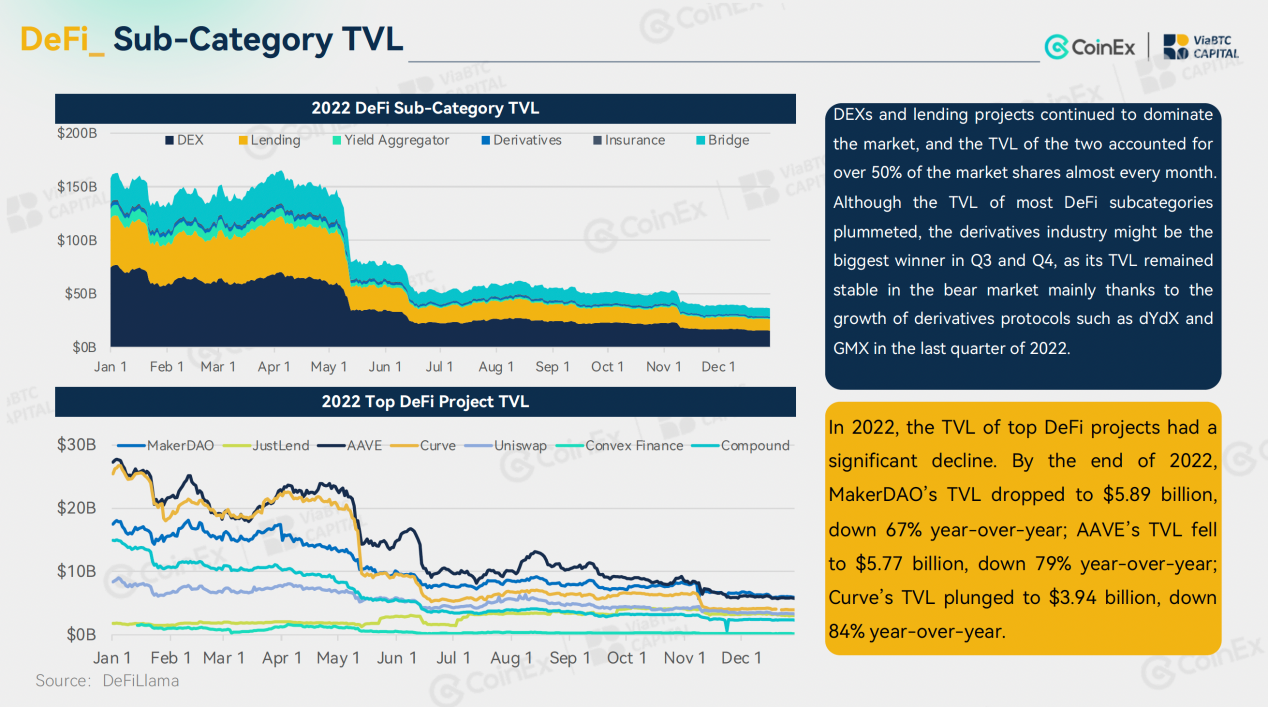

DeFi’s TVL also trended downward in 2022. In particular, during the LUNA/UST meltdown in May, mainstream coins witnessed the most spectacular crash in the history of cryptocurrencies, which was followed by a TVL collapse. Additionally, over the year, DeFi also suffered frequent hacks, which raised security concerns for DeFi. In terms of innovation, although the first two quarters of 2022 saw trending hypes about DeFi 2.0 from time to time, along with the slump of OHM and the (3, 3) meme, DeFi 2.0 was almost proven to be a completely false narrative, and the market shifted its attention back to DeFi 1.0 infrastructure projects such as Uniswap, Aave, and MakerDAO. Despite the bearish conditions, mainstream DeFi projects including AAVE and Compound managed to maintain steady operations and attracted many new users from certain CeFi projects (e.g. Celsius and FTX).

7. SocialFi

In 2022, the blockchain industry continued to explore new possibilities for SocialFi. Over the year, we saw the appearance of iconic terms like Fan Token, Soulbound Token (SBT), Web3 Social, and Decentralized Identity (DID), but the PMF (Product- Market Fit) was never identified. Despite that, the SocialFi still managed to present us with a number of star projects, including Web3 lifestyle app STEPN featuring SocialFi elements, credential network Galxe, BNB Chain domain name service SPACE ID, social graph Lens Protocol, and Web3 gamified social learning platform Hooked Protocol. Apart from that, the 2022 Qatar World Cup also helped Fan Tokens attract extensive market attention. As a result, instead of plummeting due to the bearish impact, the Fan Tokens also performed slightly better in 2022 than in 2021.

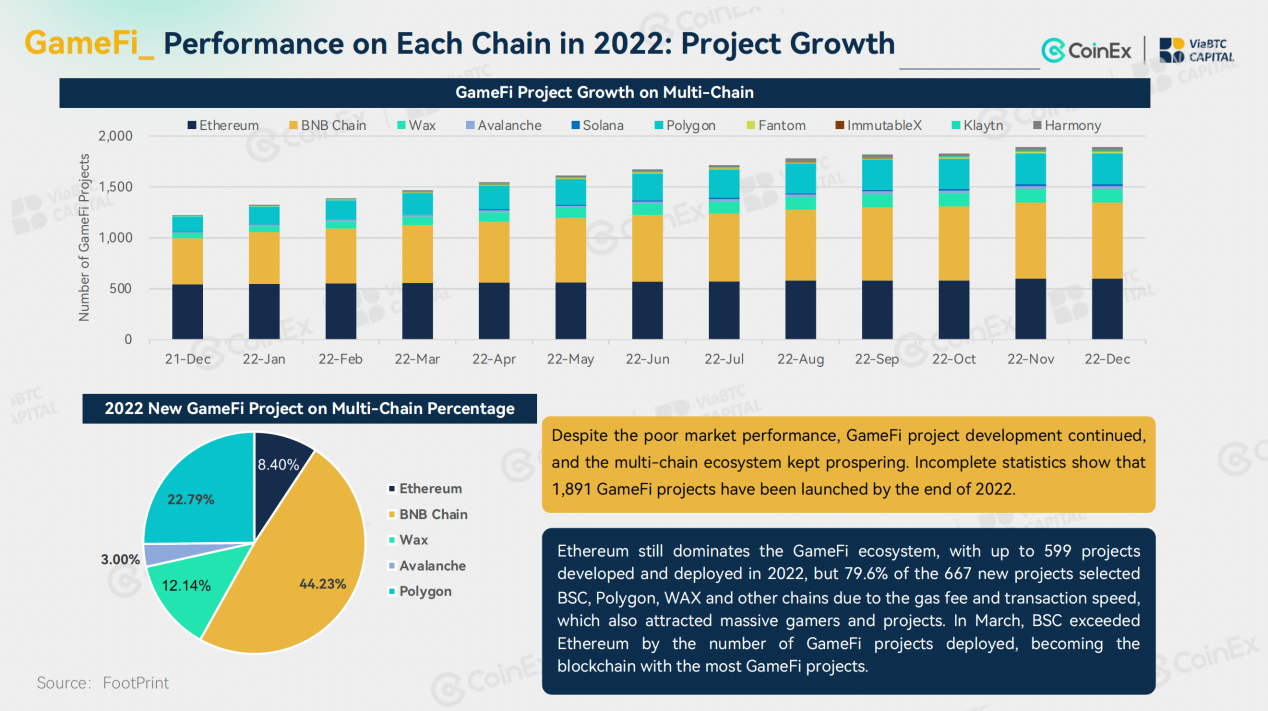

8. GameFi

2022 was also the beginning of the GameFi bear. There was no significant innovation in P2E blockchain game model. As the growth of users and trading volumes dwindled, institutional investors looked away from the P2E model. In the first half of the year, the Move-2-Earn model created by STEPN captured the spotlight with its innovative dual tokenomics and marketing approach, bringing new dynamics to GameFi. Last year, blockchain projects raised the largest funds in April, with blockchain investments totalling $6.62 billion. However, the market didn’t respond to other project teams focusing on the reality plus token model. As the multi-chain ecosystem gained growing popularity, Ethereum maintained its dominance in the GameFi ecosystem, but the growth rate of projects on Ethereum failed to match that of BNB Chain and Polygon. In addition, most chains relied heavily on their top projects, and there were still plenty of low-quality GameFi projects with a small user base, subpar interactions and low trading volumes.

9. Regulatory policies

Generally speaking, for the cryptocurrency industry, 2022 was full of ups and downs, but regulations are headed in the right direction. Over the past year, regulators in the developed world achieved a lot of progress. The United States released a regulatory framework for cryptocurrencies; the European Union initially approved the MiCA Act and the TFR Act; the United Kingdom and South Korea made progress in the establishment of the relevant organizations; Russia and Hong Kong promoted the discussion and implementation of policies for cryptocurrency mining and virtual asset securities. The turbulence that happened in the cryptocurrency industry in 2022 was partially the result of the sharp drop in funds and partially the result of regulatory loopholes and crackdowns. Last year, the bankruptcy of Terra and FTX, two top cryptocurrency projects, prompted national regulators and law enforcement agencies to further enhance their cryptocurrency oversight and investigations.

For more details, please visit the ViaBTC Capital website via the link:

For more details, please visit the ViaBTC Capital website via the link:

This is a sponsored post. Learn how to reach our audience here. Read disclaimer below.